$MSTR will Collapse, but When?

It is our opinion that even without any speculation as to BTC or wrongdoing, MSTR cannot escape insolvency.

What this is not:

-Besides highlighting that some of the high yield investment products are being marketed as suitable for retirement savings, this report does not allege any fraud, misrepresentation, or accounting irregularities.

-Bitcoin Neutral: We take NO position on the intrinsic or future value of BTC or crypto. The one exception is that we are of the opinion, consistent with consensus, that large holders of BTC may have difficulty receiving present value in USD through a large short term sale or liquidation. It is our opinion that the price of BTC only affects the WHEN not the IF.

What this is:

-This article sets forth the capital structure of MSTR and its related preferred shares provides the opinion that irrespective of what BTC does, based on this model, MSTR will become insolvent in “X” period of time.

-This event will be “amplified” because of copycat and downstream programs (savings “banks” and stablecoins) that seem to rely on MSTR remaining solvent;

-This “X” is undeterminable and subject to many variables, but calls upon experts in finance and accounting to determine when this event may take place.

-Recognizes that higher BTC valuations will extend the X, while long term price weakness may shorten the X.

-Assumes that MSTR will continue to operate as a BTC treasury company with minimal operating income or revenue outside of capital raises through its various instruments.

Executive Summary:

MSTR, a bitcoin treasury company with minimal actual income, relies upon equity and preferred stock issuance to fund its operation, bitcoin purchases, and dividend payments. In essence, it requires new investors to fund new purchases and pay old investors. Though not unique to a startup, MSTR’s business model will not generate any meaningful revenue in the near future— irrespective of the price of BTC. This means that MSTR’s survival is contingent on its ability to raise capital— easy to do during good times, not so much during hard times.

The question is how long will it last before MSTR has to sell material quantities of BTC or if it is unable to, becomes insolvent? This depends on several factors including BTC price, other income streams, payment of dividends, and investor appetite for products. If another income stream is found, then theoretically it could continue as a prosperous company. Copycats are rapidly forming that are raising money from investors to purchase MSTR products AND offer suspiciously high returns as well.

Relevant Facts:

Strategy, Inc. (MSTR), formerly know as MicroStrategy, transitioned to a Bitcoin treasury company from 2020 to 2022. Since then, it reportedly holds over 843,738 bitcoins, financed through a mix of cash flows, equity sales, and convertible debt. More recently, beginning in 2025, MSTR began issuing perpetual preferred stock with optional dividends, some payable quarterly, or on a bi-monthly basis (STRC). Although the preferred dividends are disclosed as discretionary, a review of MSTR’s social media accounts suggests that the high yields and consistent payments are a major selling point for these securities.

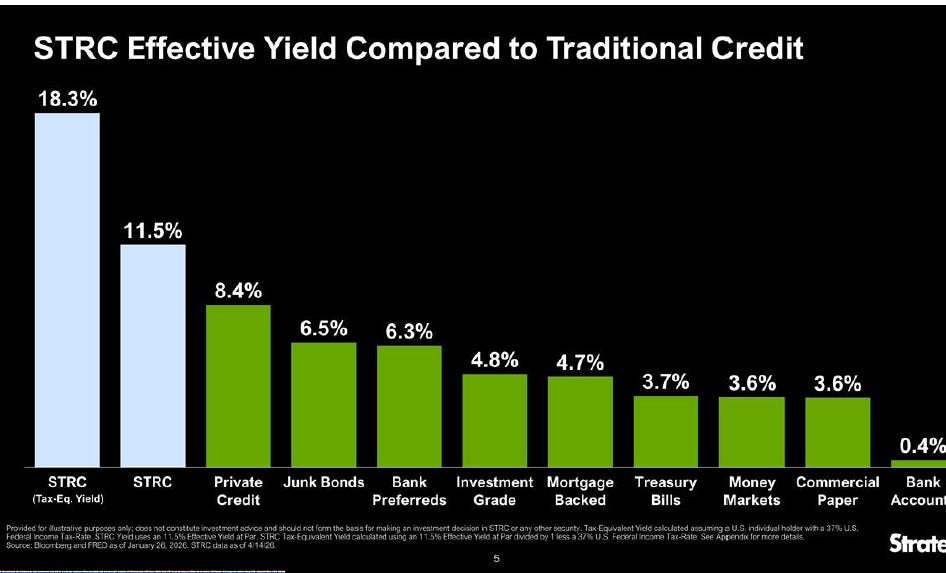

The yields are impressive, ranging from 8% to 13% depending on the product and its price. A recent presentation boasts a tax equivalent effective yield for STRC of 18.3% (current yield of 11.5%).

MSTR’s disclosures concerning revenues, expenses, and capital raises are relatively straightforward:

Product licenses, subscription services, and product support provide approximately $477 million in gross revenue with a gross profit of $327 million.

Excluding unrealized losses/gains on digital assets, operating expenses total approximately $368 million.

In 2025, MSTR recorded approximately 381 million in payments for dividends on preferred stock. See MSTR, Form 10-K, February 2025.

Preferred Shares- Transformative, until not.

In 2005, MSTR issued six series of perpetual preferred shares (STRK, STRF, STRD, STRC, and STRE) that, among other features, provide for attractive fixed or variable dividends that are payable quarterly, monthly, or in the case of STRC, bi-monthly. The most popular is STRC which has a variable interest rate adjusted to maintain a par value around $100 and yields approximately 11.5% (per year). STRD on the other hand, has a fixed payment but currently yields between 12-13% based on discount to par.

Because the dividends are discretionary these securities are not considered debt and do not obligate MSTR to pay any dividends. In addition, MSTR has set aside a reserve (financed by investors) to ensure it can pay its dividends for a set period of time. Of course, the more preferred shares that are issued, the higher the dividend payments become.

Neither the MSTR equity or preferred shares are secured by any asset. Not secured by BTC, assets, and the liquidation preferences vary. Their intrinsic value seems to be linked to BTC and its performance, but in reality it is not. To be sure, if BTC falls it might affect the ability to sell more STRC for example, or if BTC rises it might create the permissive environment to sell more STRC. Bottom line is that STRC and its progeny are speculative investment products whose existence depends on the ability to sell more STRC, equity, or other instruments.

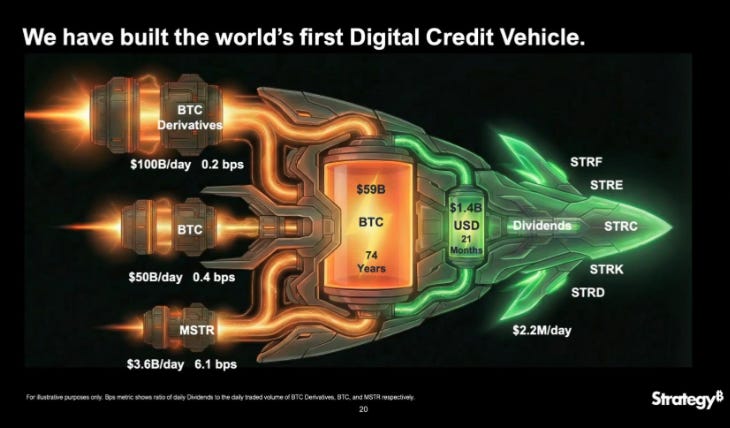

MSTR 0.00%↑ through Michael Saylor, uses the concept of “flywheel” to describe the financial engineering behind the company. It relates to the company’s premium over its Net Asset Value (NAV) based on its bitcoin holdings. This theoretically permits MSTR to raise funds through ATM offerings of equity or sale of its preferred stocks (STRC, etc.). Called a" perpetual accumulation machine” or a “self-fulfilling flywheel” this structure, in our opinion, only works when there is steady accumulation of the underlying asset and unlimited investor pool. There are cool graphics associated with this capital structure:

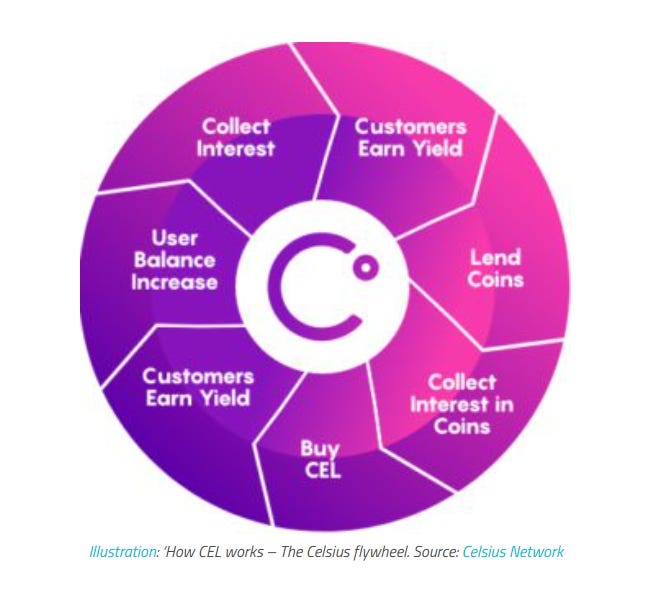

The concept of “flywheel” (although structured differently) was also used to market now defunct tokens on the Celsius Network:

CONCLUSION: Failure to Pay Dividends is Not a Default- but try raising more money that way….

MSTR correctly states that it is under no obligation to pay dividends for preferred shares (though some are cumulative). But what happens to their ability to raise capital and sell more STRC if a payment exists and/or the price of BTC plummets, even in the short term?

If capital markets dry up, as has happened in the past for reasons related to BTC or unrelated to BTC, MSTR will not be able to raise money from new investors to pay the dividends, purchase new BTC, or fund its current operations. This leaves MSTR with the options of finding a way to generate cash flow. If it sells even a portion of BTC after expounding a HODL (Hold On For Dear Life) strategy, that might create panic, even if MSTR has hinted recently it might sell BTC but then buy more. It could create newer and flashier financial products to raise money but would still require new investors. Lastly, it could pledge the BTC to secure more financing to purchase more BTC and continue to pay dividends but that would substantially increase the risk of default if BTC drops sharply in the near term.

Since the pool of new investor money is theoretically limited (this applies to any company, its pure math), MSTR will run out of money at some point. Smarter minds may be able to answer that X (“When”) question. Perhaps there are too many variables (interest rates, BTC price, economics, etc.) for anyone to answer that question but the result, assuming the continued treasury business model, it is the opinion of this article is insolvency.

Copycats “amplify” risk? What is going on here?

Perhaps smarter people can explain what is going on here. Digital credit, to the extent it is an actual thing, seems to be utilized not for capital expenditures that create new sources of income. Instead it is to issue more credit to buy BTC or pay dividends to new and old investors. MSTR’s innovative campaign to raise capital, particularly with STRC, has attracted the attention of recognized BTC treasury companies and other actors seeking to raise money. In addition, MSTR seems to be cross selling these products for reasons that are unclear.

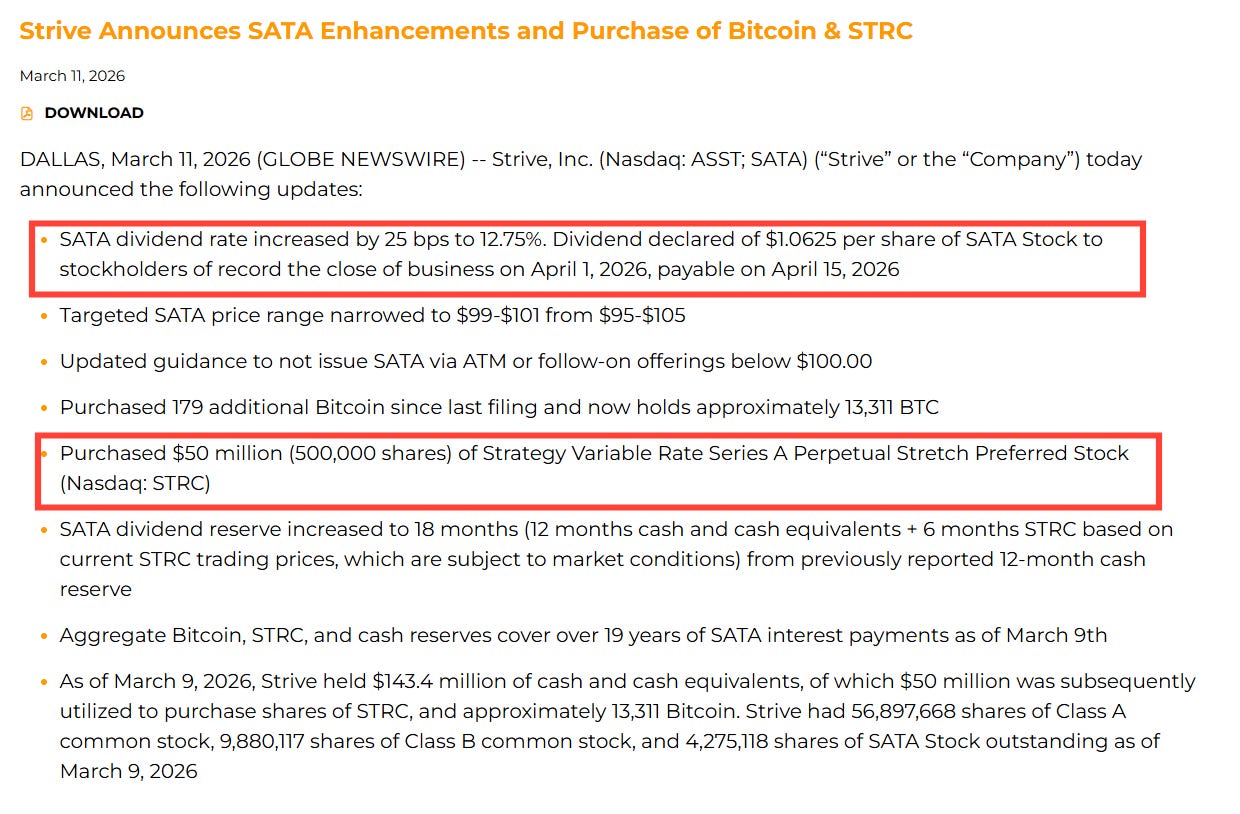

One mainstream example is Strive, Inc. ( ASST 0.00%↑), which among other investments, touts itself as a BTC treasury company. It has its own preferred stock that pays dividends listed as SATA 0.00%↑ . In March 2025, it announced that it purchased $50 million of STRC 0.00%↑ to strengthen its “treasury” and also raised the dividend on its SATA to approximately 12%.

So STRC 0.00%↑ preferred stock is being used to finance or secure additional issuance of stock and preferred dividend payments for stocks such as SATA. If STRC fails, then ASST and SATA will suffer.

A company called “APYX” boasts to be “On Track to Become the Largest Holder of $STRC” as per its X account and has been retweeted by MSTR. APYX claims to provide the first dividend backed stable coin backed by “Digital Asset Treasury (DAT) preferred equity.” In essence, APYX’s product apyUSD provides 10.23 percent APY and says will provide provide "a 13% expected APY”. These coins are back by, among other assets, STRC. As explained by an AI video posted by Apyx and reposted by Michael Saylor, APYX uses dollars to buy preferred equity such as STRC and uses that yield to attempt to provide 13% return for the holders of certain APYX coins.

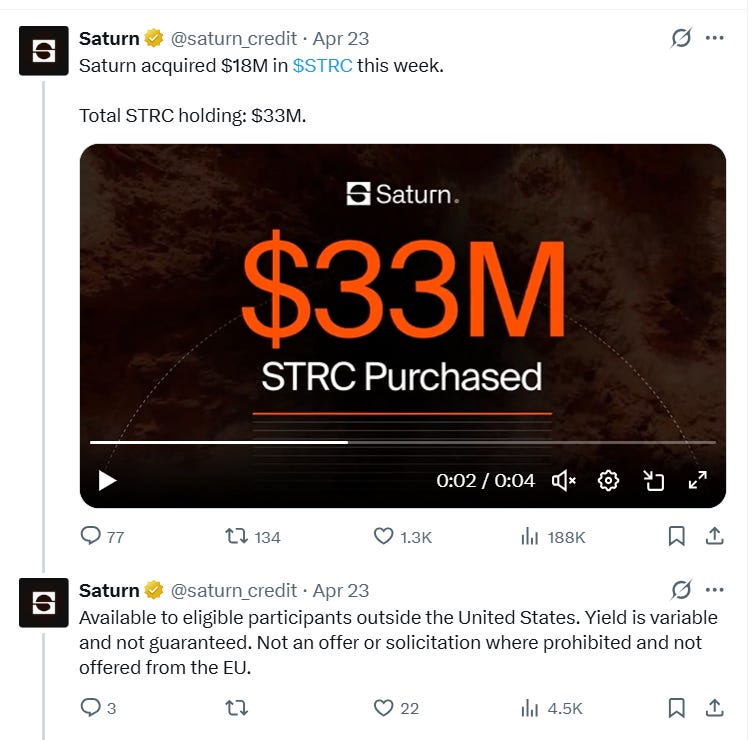

Additional companies have boasted to rely on STRC to generate yields for their investors or holders. These include Hermetica, Saturn, and Pendle. For instance, Saturn claims to offer 11% yield that is somehow backed in part by STRC.

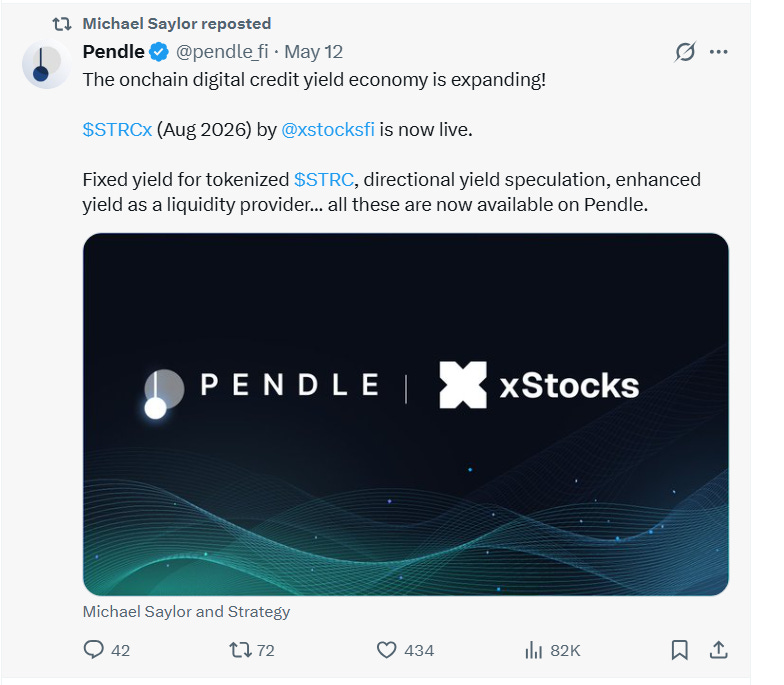

Pendle ($STRCx), allows you to trade “tokenized” STRC and the other high yielding tokens as well.

What would a possible default or skipped payment do to these companies and investors who purchased these products or invested money in hopes of receiving dividends?

CONCLUSION:

Unfortunately, it is impossible to say when money dries up to raise capital to pay older investors. There are too many variables such as interest rates, BTC price, demand from new investors, among other variables, that make that prediction. However, it is the opinion of this article that without a cash generating business model that does not rely solely on new investors, this structure has to eventually collapse.

Michael Saylor talking about these downstream "yield coins" (which is not a thing by the way). He's promoting his promoters.

https://x.com/LLuciano_BTC/status/2056736885012074566?s=20